Introduction

Personal Finance Planning is one of the most important life skills that directly impacts your financial stability, lifestyle, and future security. In simple words, it is the process of managing your income, expenses, savings, and investments in a structured way so you can achieve your financial goals without stress. Whether you are a student, a working professional, or someone starting their financial journey, understanding Personal Finance Planning can completely change how you handle money.

At its core, Personal Finance Planning is not just about saving money, but about making smart financial decisions that help you build wealth over time. It allows you to take control of your financial life instead of living paycheck to paycheck. Many people struggle financially not because they earn less, but because they lack proper planning.

When you follow a strong Personal Finance Planning strategy, you can easily track your spending, reduce unnecessary expenses, and start investing for your future. It also helps you prepare for emergencies, big life goals, and retirement. In this guide, we will break down everything step by step so even beginners can understand and apply it in real life effectively.

What is Personal Finance Planning?

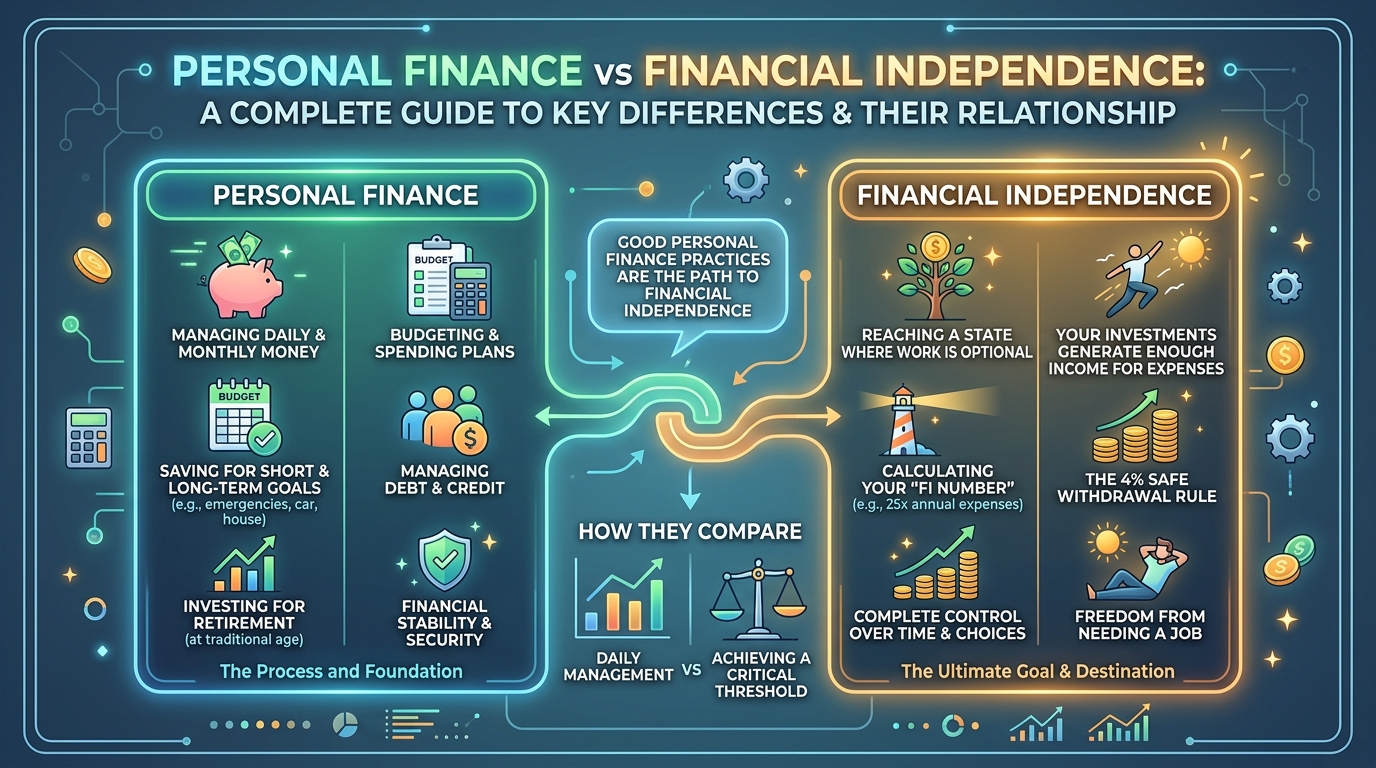

Personal Finance Planning refers to the structured approach of managing an individual’s financial resources to meet short-term and long-term goals. It includes budgeting, saving, investing, debt management, tax planning, and retirement planning. The main purpose is to ensure financial stability and growth over time.

In simple terms, Personal Finance Planning is like creating a roadmap for your money. Instead of spending randomly, you assign every unit of income a purpose. This helps you stay organized and reduces financial stress significantly. For example, you decide how much to spend on needs, wants, savings, and investments before the month begins.

Another important aspect of Personal Finance Planning is discipline. Without discipline, even the best financial plan fails. It requires consistent tracking of income and expenses and making adjustments whenever needed. Over time, this habit builds financial awareness and control.

Personal Finance Planning is not limited to rich individuals. In fact, it is more important for middle and low-income earners because it helps maximize limited resources effectively. With proper planning, anyone can improve their financial situation regardless of income level.

Why is Personal Finance Planning Important?

Personal Finance Planning plays a crucial role in achieving financial independence. Without a proper plan, people often face debt, overspending, and financial insecurity. A well-structured plan ensures that you are always prepared for both expected and unexpected financial situations.

One major reason it is important is financial security. Life is unpredictable, and emergencies can occur anytime. Personal Finance Planning ensures that you have an emergency fund to handle such situations without borrowing money.

It also helps in achieving long-term goals like buying a house, education, or retirement. When you plan your finances properly, you can allocate funds regularly toward these goals instead of struggling at the last moment. This creates financial discipline and long-term stability.

Moreover, Personal Finance Planning improves decision-making. When you understand your financial position clearly, you make better spending and investment choices. It reduces stress and gives you confidence in managing your money effectively.

Detailed Step-by-Step Guide

Step 1: Analyze Your Income

The first step in Personal Finance Planning is understanding your total income. This includes salary, business income, side earnings, or any passive income sources. Knowing your exact income helps you create a realistic financial plan.

Once you identify your income sources, calculate your monthly average. This gives you a clear picture of how much money you can allocate for expenses and savings. Without this step, financial planning cannot be effective.

Step 2: Track Your Expenses

The next step is tracking where your money goes. Divide your expenses into categories such as needs, wants, and savings. This helps you identify unnecessary spending habits.

By tracking expenses, you can easily find areas where you are overspending. This is one of the most powerful parts of Personal Finance Planning because it directly improves your saving capacity.

Step 3: Create a Budget

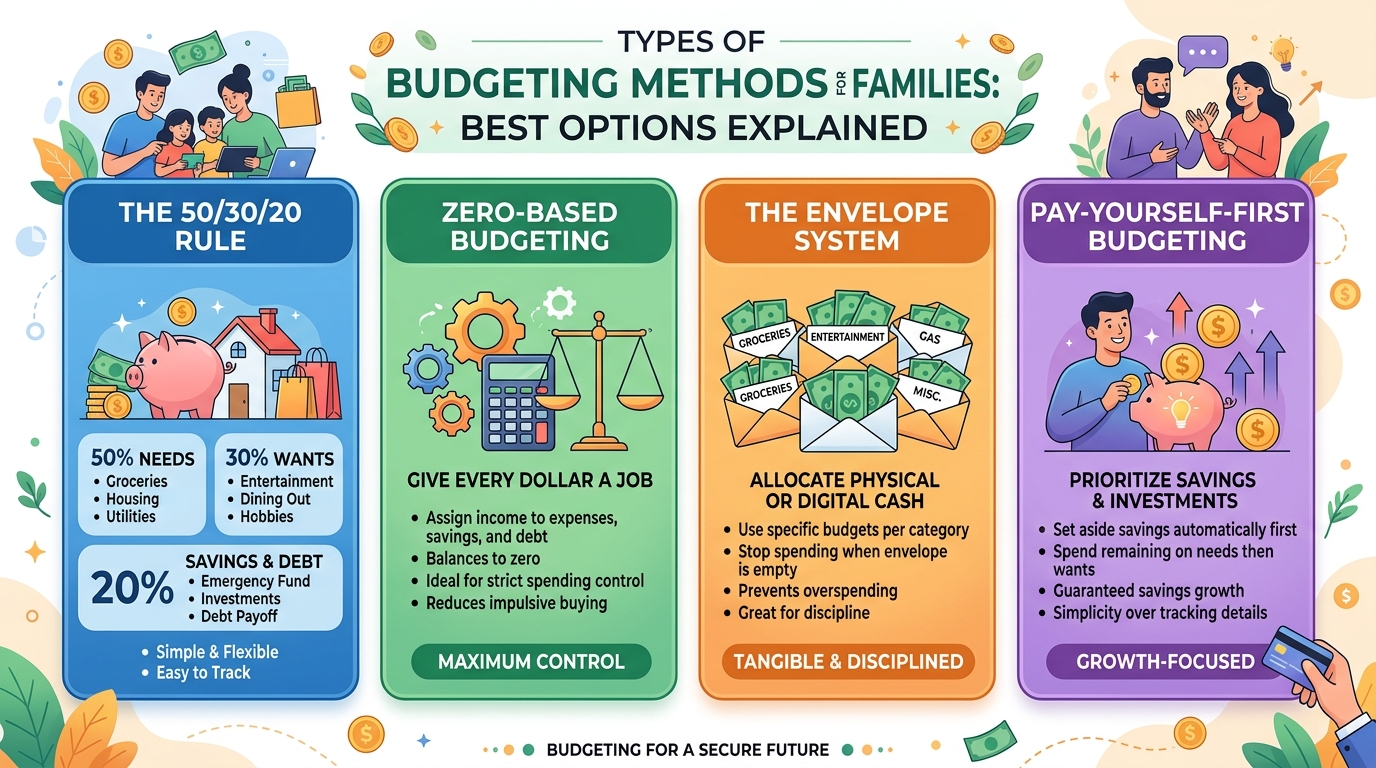

Budgeting is the backbone of Personal Finance Planning. Create a monthly budget based on your income and expenses. Assign fixed percentages to essentials, savings, and investments.

A popular method is the 50/30/20 rule, where 50% goes to needs, 30% to wants, and 20% to savings. However, you can adjust it according to your financial situation.

Step 4: Build an Emergency Fund

An emergency fund is a financial safety net. It should cover at least 3 to 6 months of your expenses. This fund protects you during job loss, medical emergencies, or unexpected situations.

Without an emergency fund, people often fall into debt. That is why it is a critical part of Personal Finance Planning.

Step 5: Start Investing

Once you have savings, the next step is investing. Investments help your money grow over time. You can explore stocks, mutual funds, or retirement accounts based on your risk level.

Investing is essential because savings alone cannot beat inflation. A good Personal Finance Planning strategy always includes long-term investment goals.

Benefits of Personal Finance Planning

- Improves financial discipline and control

- Helps achieve short-term and long-term goals

- Reduces financial stress and uncertainty

- Builds emergency preparedness

- Encourages saving and investing habits

- Helps avoid unnecessary debt

- Improves overall lifestyle quality

Disadvantages / Risks

- Requires time and consistency

- Needs financial knowledge and learning

- Can feel restrictive for some people

- Market risks in investments

- Poor planning may lead to wrong decisions

- Requires regular updates and adjustments

Common Mistakes to Avoid

One common mistake in Personal Finance Planning is not tracking expenses regularly. Without tracking, it becomes impossible to control spending. Many people also fail to set realistic financial goals, which leads to frustration and failure.

Another mistake is ignoring emergency funds. People often focus only on savings and investments but forget safety nets. Additionally, relying too much on credit cards can create unnecessary debt and financial pressure.

FAQs

1. What is Personal Finance Planning in simple words?

It is the process of managing your money through budgeting, saving, and investing to achieve financial goals.

2. Who should do Personal Finance Planning?

Everyone, regardless of income level, should follow Personal Finance Planning to manage money better.

3. Is Personal Finance Planning difficult?

No, it is simple if you follow basic steps like budgeting and tracking expenses consistently.

4. How much should I save monthly?

It depends on your income, but ideally 20% of your income should go into savings.

5. What is the first step in Personal Finance Planning?

The first step is analyzing your income and understanding your financial situation.

6. Can I start investing with a small income?

Yes, even small amounts can be invested regularly to build long-term wealth.

Expert Tips & Bonus Points

Experts suggest automating your savings so a fixed amount is transferred automatically each month. This builds consistency in Personal Finance Planning.

Another tip is to review your financial plan every few months. Income and expenses change over time, so your plan should also be updated accordingly.

Avoid emotional spending decisions. Always think before buying non-essential items. Small savings over time create big financial results.

Conclusion

Personal Finance Planning is not just a financial activity, it is a lifestyle habit that shapes your future. By managing your income, expenses, savings, and investments wisely, you can achieve financial stability and independence. Many people struggle financially not because they lack money, but because they lack planning.

When you apply Personal Finance Planning consistently, you start seeing positive changes in your financial behavior. You spend more consciously, save regularly, and invest wisely. Over time, this builds wealth and reduces financial stress.

The most important thing to remember is that Personal Finance Planning is not a one-time task. It is an ongoing process that requires discipline, patience, and consistency. Even small steps today can lead to big financial success in the future.

If you start applying the principles explained in this guide, you will gradually gain control over your finances and move toward a more secure and confident financial life.