Introduction

Borrowing money has become a normal part of modern life, especially for young adults who are starting careers, continuing education, or building independent lifestyles. From student loans and credit cards to car financing and personal loans, borrowing can help cover important expenses when savings are limited. However, without the right approach, debt can quickly become stressful and difficult to manage.

The best borrowing strategies for young adults focus on using credit wisely, understanding repayment responsibilities, and avoiding unnecessary financial pressure. Smart borrowing is not only about getting approved for loans. It also involves creating a repayment plan, improving credit habits, and choosing affordable options that support long-term financial stability.

Many young adults make financial mistakes because they borrow without fully understanding interest rates, loan terms, or monthly payment obligations. Learning effective borrowing techniques early can prevent these problems and help build a stronger financial future. This guide explains practical borrowing methods, common risks, expert tips, and useful strategies that beginners and intermediate readers can apply immediately.

What is Best Borrowing Strategies for Young Adults?

Best borrowing strategies for young adults refer to smart financial methods used to borrow money responsibly while avoiding unnecessary debt problems. These strategies help individuals choose the right type of loan, understand repayment conditions, and manage monthly payments without damaging their financial health.

Young adults often need financial support for education, transportation, housing, business ideas, or emergencies. Responsible borrowing means taking loans only when necessary, comparing lenders carefully, and borrowing amounts that can realistically be repaid. A good borrowing strategy also includes maintaining a healthy credit score, making payments on time, and avoiding high-interest debt.

Why is Best Borrowing Strategies for Young Adults Important?

Understanding borrowing strategies is important because financial decisions made during early adulthood can affect future opportunities for many years. Poor borrowing habits may lead to late payments, damaged credit scores, legal issues, and financial stress. On the other hand, responsible borrowing can help create financial stability and improve access to better opportunities.

The best borrowing strategies for young adults also help individuals develop confidence in managing money. Good credit behavior can make it easier to rent apartments, qualify for mortgages, receive lower interest rates, and access business funding later in life. Financial awareness during the early stages of adulthood creates a strong foundation for long-term success.

Detailed Step-by-Step Guide

Understand Why You Need to Borrow

Before applying for any loan or credit product, identify the exact reason for borrowing money. Many young adults borrow impulsively without evaluating whether the expense is truly necessary. Borrowing should ideally support important goals such as education, transportation, business development, or emergency needs.

Ask yourself whether the purchase can wait until you save enough money. If borrowing is necessary, determine the smallest amount required. Avoid borrowing extra money simply because lenders offer higher limits. Responsible borrowing begins with understanding genuine financial needs.

Learn the Difference Between Good Debt and Bad Debt

Not all debt is harmful. Good debt usually supports future growth or increases earning potential. Student loans, business loans, or home financing may provide long-term benefits if managed properly. These forms of debt can contribute to career advancement or asset building.

Bad debt generally involves borrowing for unnecessary purchases or luxury spending that does not improve financial stability. Expensive gadgets, impulse shopping, and entertainment purchases funded through high-interest credit cards often create financial pressure. Young adults should focus on borrowing for productive purposes rather than temporary satisfaction.

Build a Realistic Budget Before Borrowing

Creating a monthly budget is one of the most effective borrowing strategies for young adults. A budget helps track income, expenses, savings, and debt obligations. Without a budget, borrowers may struggle to manage repayments and risk missing due dates.

Start by listing all monthly income sources and fixed expenses such as rent, transportation, groceries, and utility bills. After calculating remaining funds, determine whether loan payments fit comfortably within your financial situation. Experts often recommend keeping debt payments below a manageable percentage of monthly income.

Compare Lenders Carefully

Different lenders offer different interest rates, repayment terms, fees, and loan conditions. Many young adults accept the first offer they receive without researching better alternatives. Comparing lenders can save significant amounts of money over time.

Review interest rates, annual percentage rates, repayment flexibility, penalties, and customer reviews before making a decision. Banks, credit unions, and online lenders may provide different benefits depending on the borrower’s financial profile. Taking time to compare options helps avoid expensive mistakes.

Understand Interest Rates and Loan Terms

Interest rates directly affect the total cost of borrowing. A lower interest rate usually means smaller monthly payments and reduced overall expenses. Young adults should fully understand whether rates are fixed or variable before signing agreements.

Loan terms are equally important because they determine repayment duration and monthly payment size. Shorter loan terms may have higher monthly payments but lower total interest costs. Longer repayment periods may reduce monthly pressure while increasing total borrowing costs.

Start Building Credit Responsibly

Credit history plays a major role in borrowing opportunities. Young adults with strong credit scores often receive better interest rates and easier loan approvals. Building credit responsibly requires consistent financial discipline and careful account management.

One simple strategy is using a credit card for small purchases and paying the balance in full each month. Avoid maxing out credit limits because high utilization can damage credit scores. Paying bills on time is one of the most important factors in maintaining good credit health.

Avoid Borrowing More Than You Can Repay

Many lenders approve larger loan amounts than borrowers actually need. Accepting excessive borrowing can create long-term financial stress and increase repayment difficulties. Responsible borrowers focus on affordability rather than maximum eligibility.

Calculate how much you can realistically repay each month without sacrificing essential living expenses. Consider future financial changes such as job uncertainty, education costs, or medical emergencies. Borrowing conservatively helps reduce financial risk.

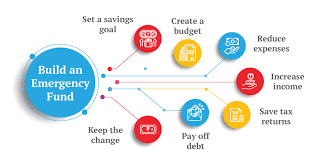

Create an Emergency Fund

An emergency fund provides financial protection during unexpected situations such as medical emergencies, job loss, or urgent repairs. Without savings, young adults may rely heavily on high-interest loans or credit cards during difficult times.

Start with small savings goals and gradually build a reserve that covers several months of expenses. Even modest emergency savings can reduce dependence on borrowing and improve overall financial security.

Prioritize High-Interest Debt Repayment

High-interest debt can grow quickly if ignored. Credit cards and payday loans often carry expensive interest charges that increase financial pressure over time. Young adults should prioritize paying off these debts as quickly as possible.

Two popular repayment methods include the avalanche method and the snowball method. The avalanche method focuses on paying debts with the highest interest rates first, while the snowball method targets smaller balances for motivation and momentum.

Read Every Agreement Carefully

Loan agreements contain important details regarding repayment schedules, penalties, fees, and borrower responsibilities. Many people skip reading contracts carefully and later face unexpected financial problems.

Take time to review every condition before signing any agreement. If something seems unclear, ask questions or seek financial guidance. Understanding contract details helps borrowers avoid hidden costs and unpleasant surprises.

Benefits of Best Borrowing Strategies for Young Adults

Using smart borrowing strategies provides several financial and personal advantages for young adults.

- Helps build a strong credit history

- Improves chances of loan approval in the future

- Reduces financial stress and repayment problems

- Encourages responsible money management habits

- Prevents unnecessary debt accumulation

- Creates better financial discipline

- Supports long-term financial goals

- Helps secure lower interest rates

- Improves financial confidence and independence

- Reduces the risk of missed payments and penalties

Disadvantages / Risks

Borrowing money without proper planning can create serious financial challenges.

- High-interest debt may become difficult to repay

- Late payments can damage credit scores

- Excessive borrowing may lead to long-term stress

- Loan defaults can result in legal consequences

- Variable interest rates may increase monthly payments

- Poor borrowing habits can affect future opportunities

- Debt dependency may reduce savings growth

- Financial emergencies can make repayments harder

- Hidden fees may increase total borrowing costs

- Impulsive borrowing can lead to unnecessary expenses

Common Mistakes to Avoid

One common mistake young adults make is borrowing money without understanding the full repayment cost. Many focus only on monthly payments while ignoring total interest expenses. This approach can lead to larger financial burdens over time.

Another major mistake is relying too heavily on credit cards for daily spending. While credit cards can help build credit history, overspending often creates debt cycles that are difficult to escape. Responsible use is essential for maintaining financial balance.

Ignoring credit score